For more than 12 years, people have been shouting about the bursting of the housing bubble on social media sites. The truth is, US housing credit looks a lot different than it did in 2005, 2006, 2007, and 2008. In fact, things look better than ever for homeowners. federal reserveOur quarterly report on household debt and credit shows why.

This time it’s not homeowners we need to worry about. Currently, renters, younger renter households, and households with lower FICO scores are exhibiting credit stress. Meanwhile, the homeowner sits beautifully and is the envy of the world.

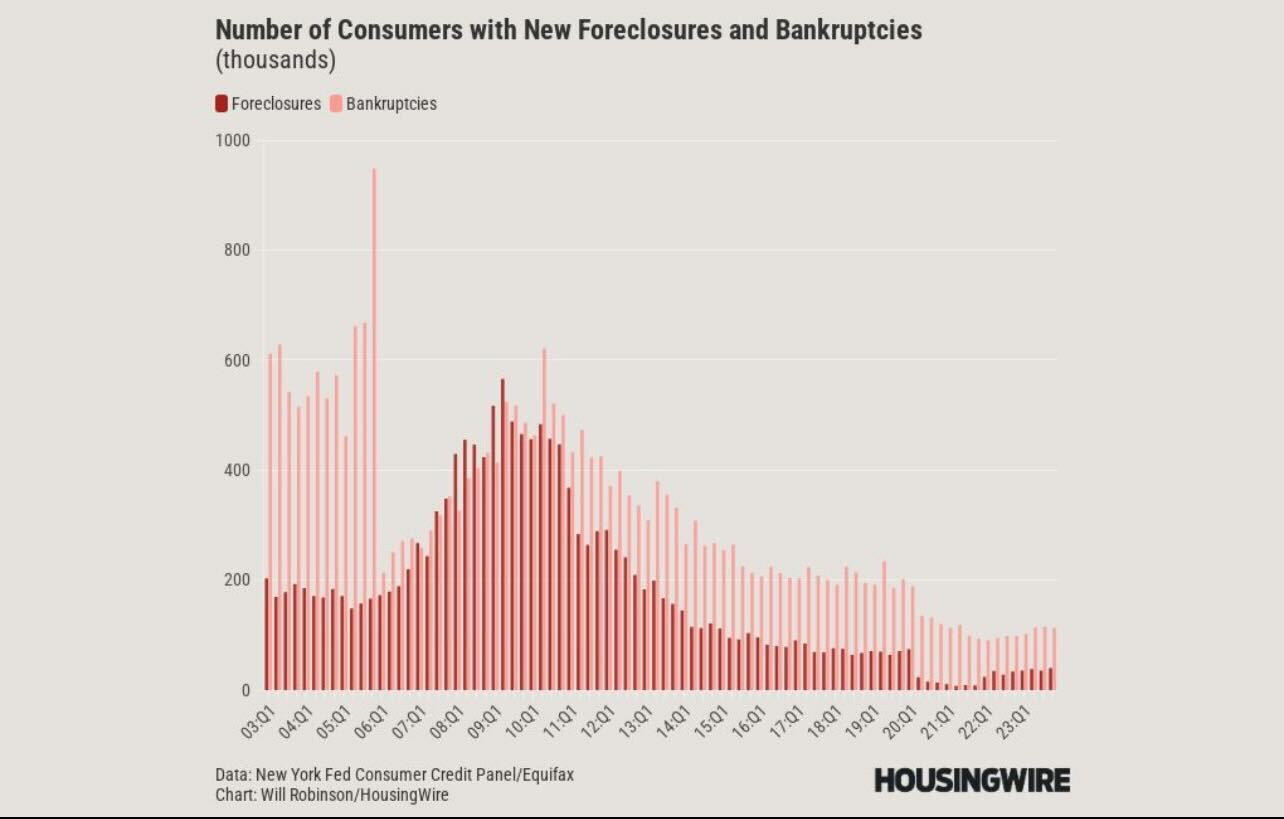

bankruptcy and foreclosure

Since 2010, the Qualified Mortgage Law has been implemented and all special loan debt structures in the system have disappeared, especially during the period of high demand from 2002 to 2005. This means that housing should only indicate financial stress when people lose their jobs and are unable to pay their mortgages. It’s not because the loan structure is a ticking time bomb.

As you can see below, data from 2005 to 2008 shows massive credit stress, but all of this was before the job-loss recession. It was for everyone to see and read. Now, the same graph shows that homeowners don’t have credit stress. So where’s the beef with those who say housing is a bubble?

From the report: About 40,000 individuals had new foreclosures listed on their credit reports, little change from the previous quarter. Since the CARES Act moratorium was lifted, the number of new foreclosures has remained at very low levels.

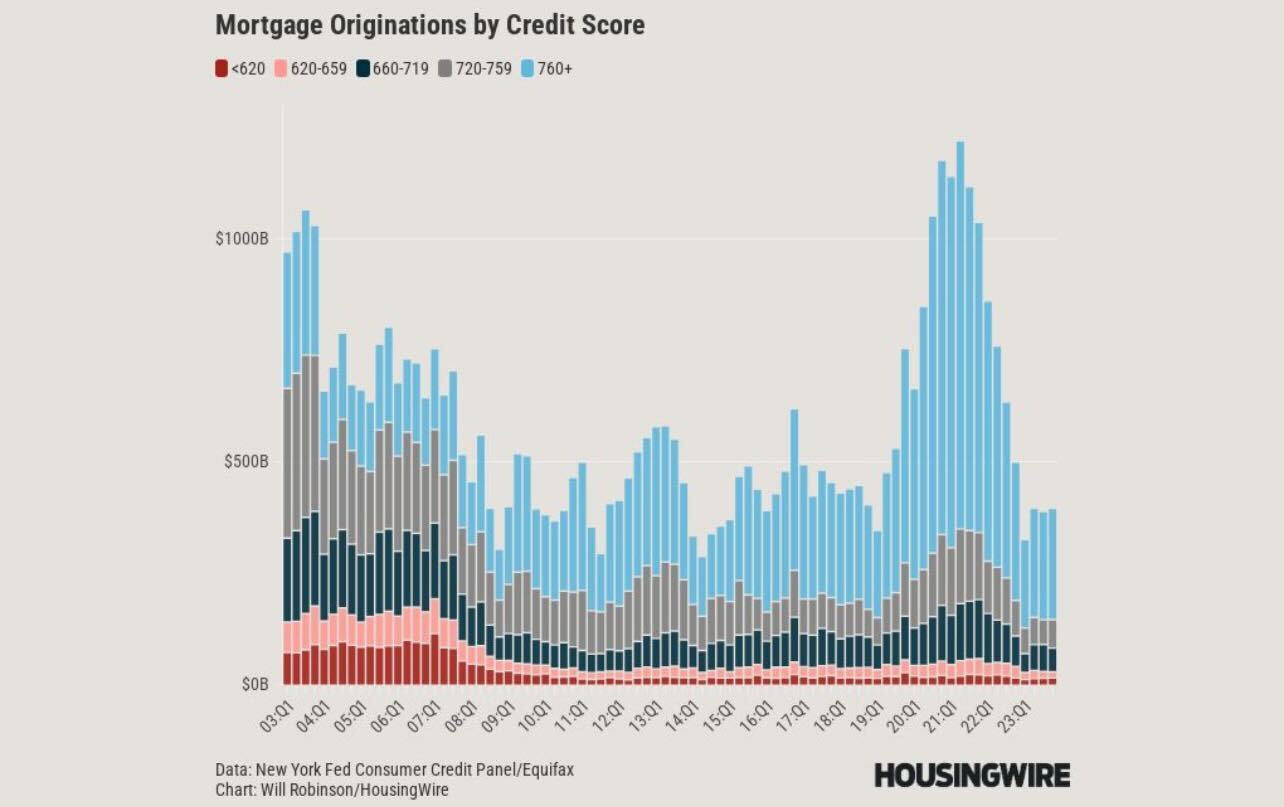

FICO score and cash flow

When I give talks at events around the country and hold up this graph, I always say, “What a beautiful graph.” That’s because since 2010, people have been taking out 30-year fixed mortgages, and each year their cash flow relative to the debt cost of their home has improved as wages have risen. Add in his three refinance waves in 2012, 2016, and 2020-2021, and you can see why homeowners are in a better position.

During periods of inflation, wages grow faster than normal, making mortgage costs much lower. Additionally, as people get older, they tend to live at home longer, and as their annual income increases, housing costs also decrease. A note on this: During COVID-19, the number of households with FICO scores of 740 or higher has exploded. Many new economists said this is FICO score inflation. But the data he has been the same since 2010. During this time, we just started more loans through purchases and refinances, so our data didn’t improve and stayed about the same.

From the report: The median credit score for newly originated mortgages was flat at 770, while the median credit score for newly originated auto loans was 720, up 1 point from the previous quarter.

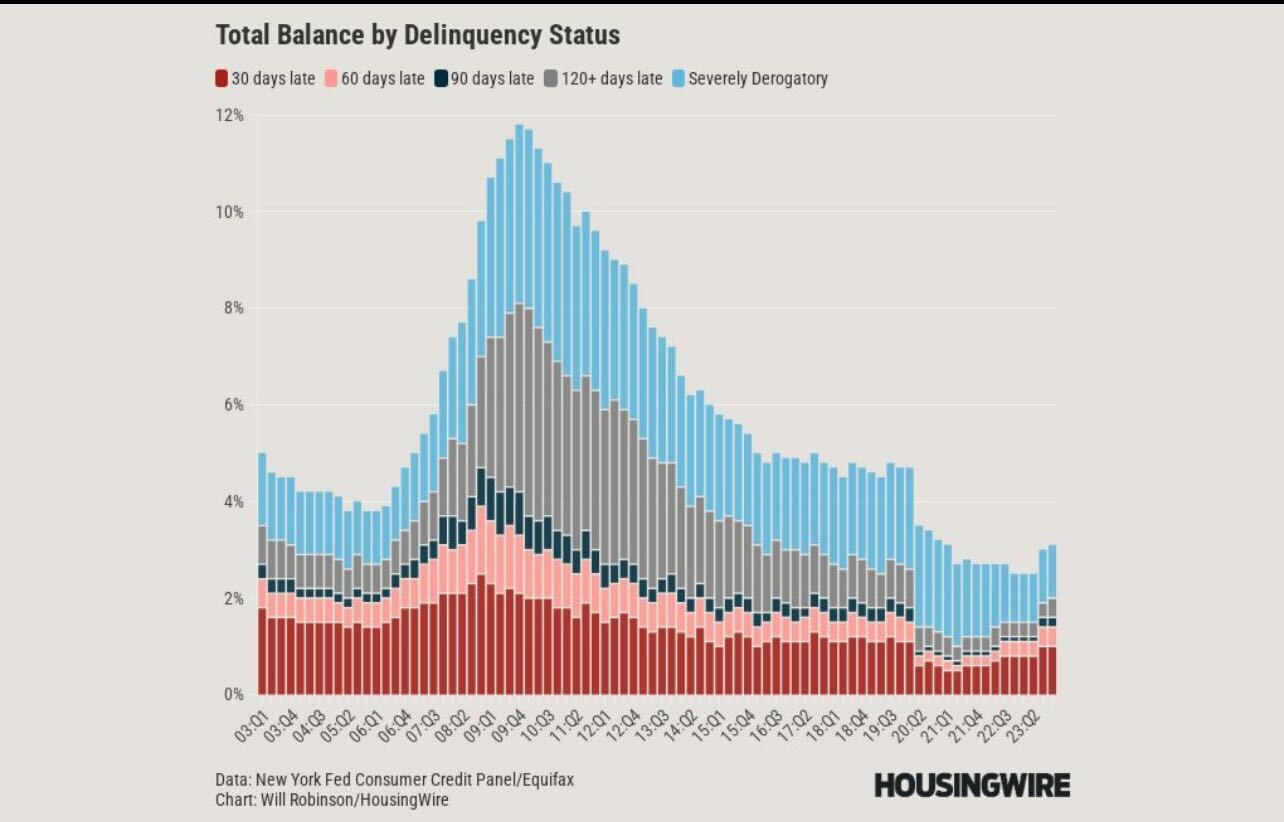

Delinquency status

When the next job-loss recession arrives, everyone should expect credit stress on housing to begin to rise. Every month, people get laid off and can’t find work right away. This is why unemployment claims never go to zero and are delayed by a certain amount of 30-60 days each month. However, as we continue to see credit delinquency data near record lows and homeowners’ household finances in such good shape, credit stress data is likely to be similar to what we saw in 2008. It probably won’t happen.

Over 40% of American homes don’t even have a mortgage and have a lot of nested equity, so in the worst case scenario, many homeowners who bought a home between 2010 and 2020 will have a lot of equity. You own it and can sell it. Keep in mind that the foreclosure process typically takes 9 to 18 months from start to finish. This means that our in-house legal process ensures that homes are brought to market. This is very different from his 2008, when he had credit stress building up over four years in the system.

From the report: Mortgage early delinquency rates increased by 0.2 percentage points but remain low by historical standards.

If you read the graph and explanation, you’ll see why this is not a 2008 home. However, credit stress is visible in the data for younger households and those with lower FICO scores. The people Jerome Powell says he wants to help at every meeting are showing credit stress.

The Fed missed it when the credit stress of the housing bubble was evident heading into 2008, but now, with some preoccupation with 1970s inflation, the Fed is making homeownership more difficult by keeping policy too restrictive. They turn a blind eye to people other than themselves. A model that no longer exists. Or, as we’ve been saying since 2022, they’re old and slow. It’s the nature of the beast.