DUBLIN, Jan. 8, 2024 (GLOBE NEWSWIRE) — Defense Market by Platform (Land, Naval, Airborne), Solution (Communications Network, Chipset, Core Network), End User, Network Type, Installation and Region 5G in North America, Europe, Asia Pacific, LA, MEA – Global Forecast to 2028 report added ResearchAndMarkets.com Recruitment.

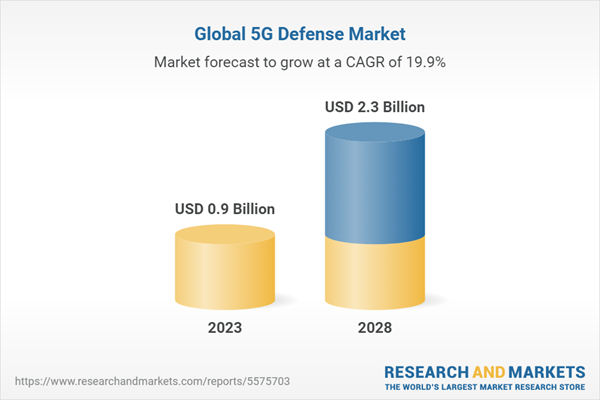

The defense 5G market is estimated to be USD 900 million in 2023 and USD 2.3 billion by 2028, at a CAGR of 19.9% from 2023 to 2028. Due to many factors, the global market for 5G in the defense sector is expanding significantly.

The fifth generation of cellular networks, known as 5G, represents a significant advancement in telecommunications technology. Delivering up to 100x faster speeds than the previous generation of his 4G, it offers unprecedented possibilities for individuals and businesses alike. 5G offers increased connection speeds, significantly lower latency, and increased bandwidth that is accelerating social progress and reshaping various industries. This transformation has significantly improved people’s daily experiences.

Market growth is driven by the increasing demand for low-latency networks that can improve more reliable and faster communications with unmanned systems, including command, control, communications, computers, intelligence, surveillance, and reconnaissance (C4ISR) systems, and drones. It is propelled by (UAVs), unmanned ground vehicles (UGVs), and autonomous naval vessels. Faster data rates and lower latency can support AR and VR applications for training simulations and battlefield data visualization.

Millimeter waves in the 5G spectrum, characterized by high frequencies and short wavelengths, facilitate real-time communications in areas with high security requirements, such as military bases and command posts. Conversely, the lower frequency, longer wavelength spectrum can be utilized for long-distance communication needs.

There are many factors driving the growth of land-based 5G in the defense market. These include the growing demand for secure and reliable communications, the growing use of unmanned vehicles, the need for global coverage, and the development of new technologies. Ground 5G in the defense market This growth reflects the evolving strategic, operational and technological landscape of modern ground warfare. As the nature of conflicts and technological paradigms change, so too will the requirements and solutions in the terrestrial 5G technology field.

Communications Infrastructure: 5G Largest Segment in Defense Market by Solution in 2023

The small cell segment due to the growth of communication networks is believed to be due to the increase in disposable income in various economies, coupled with the increased consumption of high data rates. Small cells also enhance signal broadcast across high bands, improving signal performance. For example, his 5G midband signal from an outdoor antenna may not provide consistent reliability indoors. By using strategically placed small cells, signal reliability and performance can be significantly improved.

Ultra Reliable Low Latency Communications (URLLC): 5G will have the second largest share by network type segment in the defense market in 2023.

Ultra-reliable low-latency communications (URLLC) is a service category supported by 5G in the defense sector, which brings significant benefits to a variety of industries and applications. By leveraging a satellite-based network, URLLC provides highly reliable connectivity free of terrestrial interference, ensuring consistent availability of critical applications. 5G in defense enables low-latency connectivity. This is very important for applications where even small delays can have a large impact.

For example, industrial automation can benefit from this technology by increasing efficiency and productivity through real-time communication between sensors and actuators. Similarly, self-driving cars can operate safely and efficiently by leveraging 5G for defense, enabling seamless and instantaneous communication between the vehicle and the surrounding infrastructure. These examples highlight the transformative potential of 5G in defense to enable a wide range of innovative URLLC applications.

5G Largest Segment by End User in Defense Market in 2023: Military

The military field of 5G in the defense market has many applications, including: 5G’s low latency is essential for the operation of drones (UAVs), unmanned ground vehicles (UGVs), and other robotic systems.

These systems can be used for surveillance, bomb disposal, and even combat. 5G supports streaming high-definition video feeds from reconnaissance platforms, providing timely information and a comprehensive view of the battlefield. Real-time data flow powered by 5G will significantly improve situational awareness and decision-making, allowing commanders to quickly respond to changing war situations. With 5G, soldiers can be equipped with wearable devices that monitor vital signs, location, and environmental conditions, and transmit data in real-time to medical centers and command centers.

Medium Operating Frequency: 5G Largest Share of Defense Market by Operating Frequency Segment in 2023. Based on the operating frequency segment, the 5G in defense market is classified into low, medium, and high. Based on the numbers, medium operating frequencies have secured the largest market share in their use. Mid-band 5G operates in the frequency range of 1.7 GHz to 2.5 GHz. It offers the best combination of both speed and coverage, providing connectivity to a wide area with speeds from 100 to 900 Mbps.

Mid-band 5G will be particularly beneficial not only for self-driving cars but also for applications such as enhanced mobile broadband (eMBB) and ultra-reliable low-latency communications. Additionally, we support sectors such as media and entertainment, healthcare, smart urban planning, and intelligent agriculture.

New Implementation Segment: 5G Defense Market Segment to Grow at Fastest CAGR During Forecast Period (by Installations)

The new implementation market refers to the independent 5G network market. New implementations of 5G include both new radios and cores. This network provides users with an end-to-end 5G experience. This network can interoperate with existing 4G or LTE networks to provide service continuity between the two network generations. The 5G core uses a cloud-aligned service-based architecture (SBA) that supports control plane function interaction, reusability, flexible connectivity, and service discovery across all functions.

Deploying a new implementation architecture network can be capital intensive. This includes all use cases, including those that rely on eMBB and URLLC and mMTC. It has an operating data rate of 20 Gbps or 10 Gbps, a latency of 1 ms (relatively lower than NSA), and a network density of 1 million devices/km2.

Japan is expected to account for the highest CAGR in 5G in the defense market in the forecast year.

The Japanese government has been active in developing policies and strategies to ensure the rapid deployment of 5G networks. The Ministry of Internal Affairs and Communications (MIC) has played a key role in setting 5G guidelines and frequency allocation. In April 2022, the Japanese government set an ambitious 5G goal of providing 5G networks to 99% of the population by 2030. This effort is primarily overseen by the Ministry of Internal Affairs and Communications (MIC).

In 2019, the Ministry of Internal Affairs and Communications granted access to 5G spectrum to major carriers, including NTT Docomo, KDDI au, Softbank, and new entrant Rakuten Mobile, paving the way for 5G infrastructure development. By March 2021, all these carriers had launched commercial 5G services in all prefectures in Japan. As of 2022, over 20,000 mmWave gNodeBs have been deployed by these four major service providers.

Additionally, additional nodes are promised to be installed in line with obligations set by the MIC, with completion targeted for early 2024. The agreement highlights cooperation in 5G technology, artificial intelligence, and other key areas. The two strategic allies are determined to expand their partnership with a focus on advancing supply chain initiatives within the Indo-Pacific region.

competitive environment

Prominent companies in the defense 5G market are Ericsson (Sweden), Huawei (China), Nokia Networks (Finland), Samsung Electronics (South Korea), NEC (Japan), Thales Group (France), L3Harris Technologies, Inc is. (USA), Raytheon Technologies (USA), Ligado Networks (USA), and Wind River Systems, Inc. (USA).

Key attributes:

| report attributes | detail |

| number of pages | 250 |

| Forecast period | 2023-2028 |

| Estimated market value in 2023 (USD) | 900 million dollars |

| Projected market value to 2028 (USD) | $2.3 billion |

| compound annual growth rate | 19.9% |

| Target area | global |

premium insights

- Market-driven IoT, enhanced AR and VR, advanced autonomous systems, and increasing use of 5G for cybersecurity

- Land segment will lead the market from 2023 to 2028

- Telecommunications network sector captures the largest market share during the forecast period

- Military sector will account for the largest market share during the forecast period

- Embb segment leads the market during the forecast period

- New implementation segment captures larger market share than upgrade segment during forecast period

- Low segment will have the largest market share during the forecast period

case study analysis

- Critical Communication (Cc) and Ultra Reliable Low Latency Communication (Urllc)

- Successfully demonstrated under the US Department of Defense’s 5G-To-Next G initiative

- 5G emergency rescue platform

Market trend

driver

- Use of 5G in situational awareness activities

- Technological innovation in 5G networks

- Increased use of autonomous and connected devices integrated with 5G

- Migrate from legacy systems to cloud-based solutions

- Growing demand for high-speed, low-latency connections

restraints

- Heavy investment in the early stages

- Lack of established protocols and standards

opportunity

- Increased defense budget for research and development and technological advances in unmanned systems

- The rise of virtual networking architectures

assignment

- Complexity of spectrum management

Trends and disruptions impacting your business

- 5G revenue trends and new revenue sources for defense manufacturers

- Recession impact analysis

ecosystem analysis

- prominent companies

- Private and small businesses

user

- technical analysis

- massive mimo

- Non-standalone 5G network

industry trends

Key technology trends for 5G in the defense market

- Augmented reality (Ar) and virtual reality (VR)

- edge computing

- cloud computing

- small cell network

Impact of megatrends

- Real-time data collection using the Internet of Things

- Integrating artificial intelligence into defense solutions

Company Profile

key player

- Ericsson

- nokia

- NEC

- Samsung Electronics Co., Ltd.

- huawei

- Thales Group

- Raytheon Technologies Corporation

- intelsat

- Qualcomm Corporation

- Cisco Systems Corporation

- Verizon Communications Inc.

- Deutsche Telekom AG

- orange SA

- Gogo Co., Ltd.

- Ligado Networks

- Wind River Systems Corporation

- Analog Devices, Inc.

- Intel Corporation

- L3 Harris Technologies Co., Ltd.

other players

- Conva Telecom

- Starlight Technologies Co., Ltd.

- T-Mobile US, Inc.

- Telecom Italia

- marvel

- Mediatech Co., Ltd.

For more information on this report, please visit https://www.researchandmarkets.com/r/k41wy9.

About ResearchAndMarkets.com

ResearchAndMarkets.com is the world’s leading source of international market research reports and market data. We provide the latest data on international and regional markets, key industries, top companies, new products and latest trends.