Atlanta Federal Reserve officials said the Fed’s 2023 survey results confirm the growing demand for instant payments.

Claire Green, a payments risk specialist at the Federal Reserve Bank of Atlanta, shared an analysis of various data points included in last year’s Household Economics and Decision Making Survey. In a Feb. 5 blog post, he said that taken together, this data proves that consumers are accepting payments as quickly as possible.

According to him, Exhibit A concerns virtual currencies. One-fifth of respondents who use cryptocurrencies say the top reason for adopting digital currencies is the ability to “send money faster.”

Green noted that the 27% increase in same-day ACH payments last year is similar to the sharp decline in the use of checks and money orders, from 47% in 2019 to 31% in 2022. He said this is further evidence of prompt payments. He also pointed to another Fed survey from 2022 that found 75% of consumers said they use faster payment methods such as PayPal and Square Cash.

For Green, these statistics help make the decisive case that consumers prefer instant payments.

“Even unbanked households have moved from paper methods to arguably faster digital methods,” she writes.

For regular readers of PYMNTS Intelligence, Green’s ruling may not be news to you. Last November, we published a joint study, “Measuring Consumer Satisfaction with Instant Payouts,” conducted by PYMNTS Intelligence and Ingo Payments. This study examined cash distribution amounts among US consumers and confirmed that most consumers are choosing instant his payouts en masse.

A November survey of more than 3,900 consumers across the U.S. found that 72% of respondents said yes if given the opportunity to receive an immediate payment. Meanwhile, 62% said they would choose to pay immediately if given the opportunity.

A November survey of more than 3,900 consumers across the U.S. found that 72% of respondents said yes if given the opportunity to receive an immediate payment. Meanwhile, 62% said they would choose to pay immediately if given the opportunity.

Note that these preferences are not limited to wages. In addition to income, the study also considered other sources of income, including Social Security payments, tax refunds, insurance payments, freelance income, loan payments, and more. Six out of 10 U.S. consumers receive some form of payment from a business or government, averaging $34,000 annually.

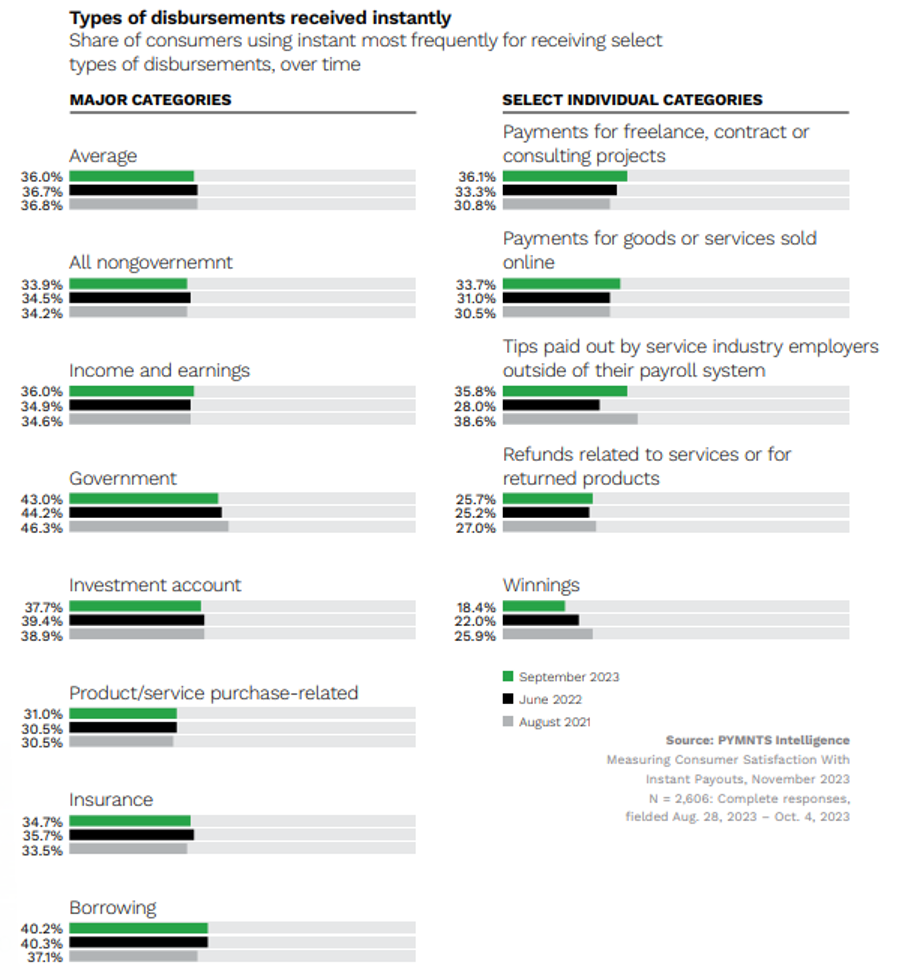

Additionally, while the majority of recipients admit that they prefer instant payments, some groups are more open to instant payments than others. For example, 36% of people who earn freelance or consulting income prefer immediate payment, an increase of 16% from two years ago.

But recipients aren’t the only ones who see value in faster payments. The payers, the people who distribute the funds, know that too. “Measuring Consumer Satisfaction with Instant Payments” found that consumers are making fewer payments. At the time this report was compiled, consumers were receiving, on average, nine payments, down from his 14 payments a year earlier. This decline suggests that payers are consolidating payments to reduce payment frequency, likely due to inefficiencies in traditional distribution methods.

The study also found that instant payments significantly improve customer satisfaction. This can benefit both the payer and receiver.

The availability of instant payments increases consumer satisfaction by 11%, and consumers are nearly twice as likely to remain a customer if instant payments are offered for free (because of convenience). Even though many people say they are willing to pay for it). The survey also found that 78% of consumers reported being “very satisfied” with receiving payments through instant payments.

But even the 78% figure may not fully reflect the public’s enthusiasm for immediate payments. Another PYMNTS Intelligence study from last year, “How Open Banking Can Deliver Faster and Easier Payments to Consumers” (conducted in collaboration with Trustly) found that respondents who were “very satisfied” or “very satisfied” when they received their funds received their funds. The number of consumers who answered “very satisfied” was revealed. The almost real rate he rose to 92%.