")

Javier Lizarazo Guerra/iStock, Getty Images

Last time I wrote Advanced Micro Devices (Nasdaq:AMD) recommended buying if the stock price falls to $75-80 per share on March 30, 2023, and holding at $98 per share. My thesis is, The company is on the road to recovery, and while it will take time for the two cyclical segments to bottom out, overall the company has the strength to continue to perform well in the coming years. I bought the stock in the mid-80s back in May, and then added another $100 more, believing there was an opportunity in AI data center revenues. Here are the main reasons I liked the company in my last article:

It has made great strides in the data center and embedded sectors, capturing a significant share of the data center market alongside struggling Intel. market.

While Generational AI has a small presence at present, it is set to grow significantly with its new processor, the MI300, which is designed for data center clients who need supercomputing and other high-performance computing applications.

AMD’s prowess in hybrid computing with its Accelerated Processing Units (APUs) is a major factor in putting the company at the forefront of next-generation AI for the data center.

One of the biggest competitive advantages from this merger is AMD’s ability to offer customized solutions from a much broader repertoire that includes the use of FPGAs, adaptive SOCs, DPUs and a common software platform.

Not only that, but I believe in all of these reasons and am excited to see AI data center revenues growing at a staggering $4.5 billion per year.

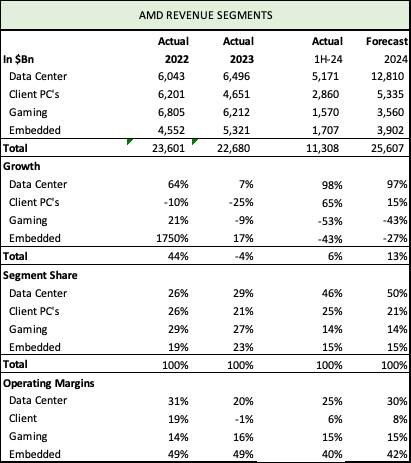

Revenue Segment

For AMD to succeed, all four segments need to grow, or the cyclical segments will destroy any positive momentum in AI. At $4.5 billion annually, AI sales represent just 18% of total revenue.

AMD Revenue Segment (AMD, Seeking Alpha, Fountainhead)

Data Centres: The first half of the year saw a remarkable recovery with total revenue up 6% and data center revenue up 97%. Shipments of the MI300X, which competes with the Nvidia (NVDA) Hopper series, surged and, like Nvidia, faced supply constraints. At this utilization rate, management was confident of $4.5 billion in utilization in 2024. This may be a conservative estimate if supply recovers. Data center generated 25% operating margin, but this number is low as AMD is taking advantage of lower price points to penetrate hyperscaler clients’ data centers, but will improve over time.

client: Another piece of good news was a 14% increase in average prices for mobile and desktop processors. Coupled with a 44% increase in shipments, client revenues increased 65% year over year to $2.9 billion. Operating margins also turned positive, at 6%, after declining in 2023.

game: The gaming industry continues to struggle in the first half of 2024, with a big 53% drop due to weak console sales at the end of a five-year cycle. Q2 was even worse, with a 59% drop despite being in a seasonally weak period, and it will take some time for the industry to clear inventory and return to growth. Nvidia grew gaming revenue by 18% in the April 2024 quarter, but only sees growth of 8% in the second quarter of 2025 and 5% overall in the January 2025 quarter. So we’re not out of the woods yet.

embedded: Another weak quarter, down 41%, with a slight improvement in the first half overall, down 43%, but the big problem for the embedded division is the post-COVID-19 inventory glut, which has not yet been resolved but is expected to improve in the second half of 2024, resulting in an overall decline of 17%, most of which comes with costs, with operating margins falling to 40% from 49% last year.

Company-wideIn the first six months, AMD has seen a turnaround. In addition to 6% growth, AMD has also improved its margins, with gross margins improving from 45% to 48% in the first half of 2023 and further to 49% in the second quarter, a great sign in the right direction.

GAAP operating income increased to $305 million from a loss of $165 million, with the majority of the $269 million coming in the second quarter. While margins are tight, they’re an improvement over AMD’s worst year in recent history, 2023, when the company made just $401 million on sales of $22.68 billion.

While we applaud the impressive progress in the data center sector, three other areas must bounce back for AMD to approach a reasonable valuation.

AI — Data Center

AMD is expected to exceed $4.5 billion in AI revenue in 2024, accounting for about 35% of the total data center revenue of $12.8 billion. In Q2 2024, GPUs accounted for $1 billion and CPUs and others for $1.8 billion of the total data center revenue of $2.8 billion. This is the first time that GPUs have accounted for such a large share of data center revenue, and they are AMD’s fastest growing product in history, which bodes well for the future as AI demand continues to improve. AMD could have sold more if it weren’t for supply constraints, but that will improve over the next two years. Another notable positive is that Nvidia’s price hikes will work in AMD’s favor. AMD can also raise prices as a second supplier, as they are discounted below Nvidia’s Hopper and Blackwell series. AMD’s average price is about $15,000, compared to Nvidia’s over $30,000.

AMD has different AI strengths than Nvidia. The MI300x series has larger memory and is better suited for inference. The thicker HBM memory in the MI300X makes it a preferable choice over the H100 when fewer devices are needed for the job. It’s cheaper and more efficient to use an AMD GPU.

Hyperscalers like Amazon (AMZN), Alphabet (GOOGL) (GOOG), Meta Platforms (META), and Microsoft (MSFT) are spending like drunks. The demand for GPUs and CPUs in data centers is huge. In an interview with Next Platform, Timothy Prickett Morgan and Forrest Norrod, general manager of AMD’s data center business, said, emphasis mine…

Forest Norrod: I understand that. The scale of what’s being considered is mind-blowing. Now, will all of this come to fruition? I don’t know. But here are some public reports: Very sober people are considering spending tens or even hundreds of billions of dollars on training clusters.

But some of the training clusters being considered are downright surprising…

About TPPM: What’s the biggest AI training cluster that someone is seriously working on? You don’t have to name names. Someone could come to you and say, Apparently the MI500 requires 1.2 million GPUs.

Forest Norrod: Is it within that range? Yes.

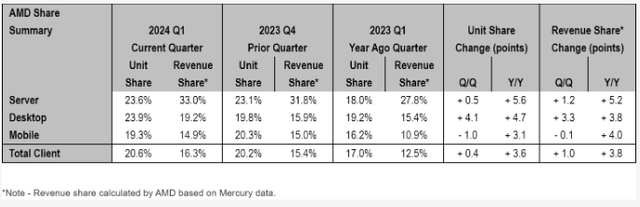

With its EPYC CPUs, AMD took a 5.6% share from Intel (INTC) in data center servers in Q1 2024, which would have grown from 18% in Q1 2023 to 23.6% in Q1 2024. Even more impressive is the revenue share, which increased by 10 percentage points to 33%, clearly indicating higher demand for EPYC.

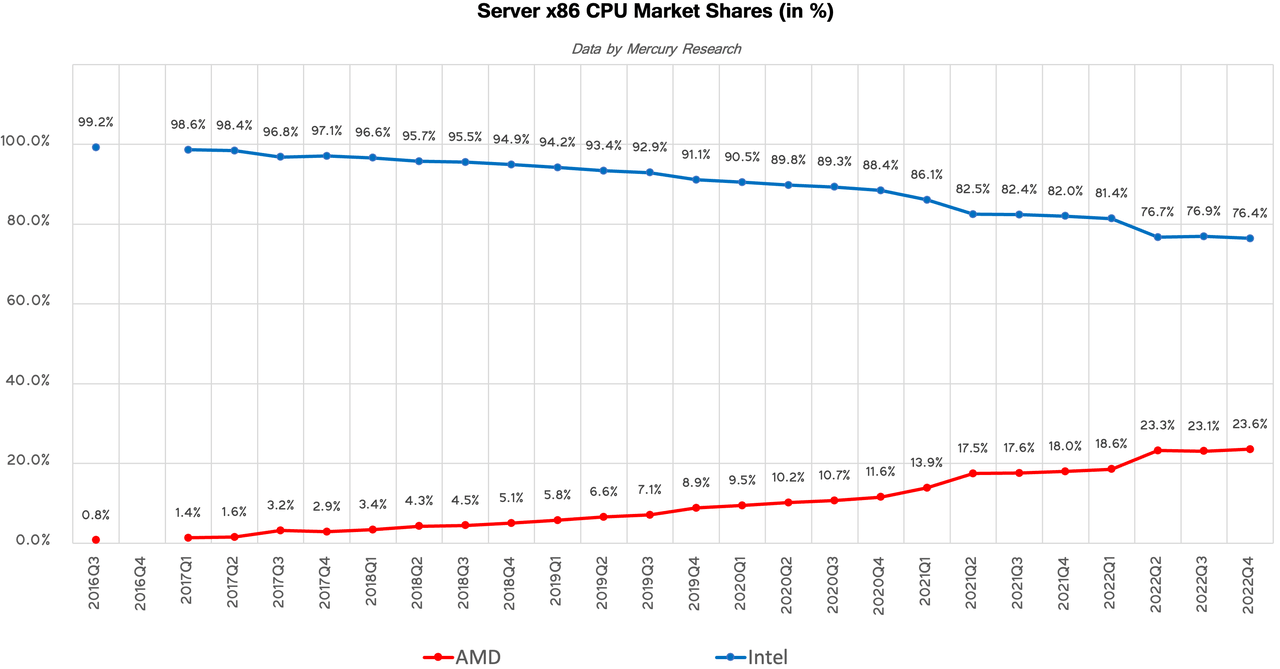

Data Center CPU Market Share (Tom’s Hardware)

Historically, AMD has grown its server market share in both units and revenue. This can be seen in the steady progress below. 23.6% at the end of Q1 2024 is up from just 1.4% in Q1 2017. This is a notable performance against a giant incumbent. In 2017, Intel had 12x revenue of $62.7B compared to AMD’s $5B. In this growing market, AMD is gaining momentum. Cloud deployments to hyperscalers are key. Hyperscalers are looking for more power and AMD is gaining momentum with high-end expensive machines with advanced CPUs. Intel lacks products that can compete with AMD’s 96-core and 128-core processors. If this trend continues, it will be a battle AMD will lose.

PC Market Share (AnandoTech)

AI — PC

AMD’s revenue has grown fourfold over the past decade, from $5.5 billion to more than $22 billion, while Intel (INTC) has stagnated at $56 billion over the same period.

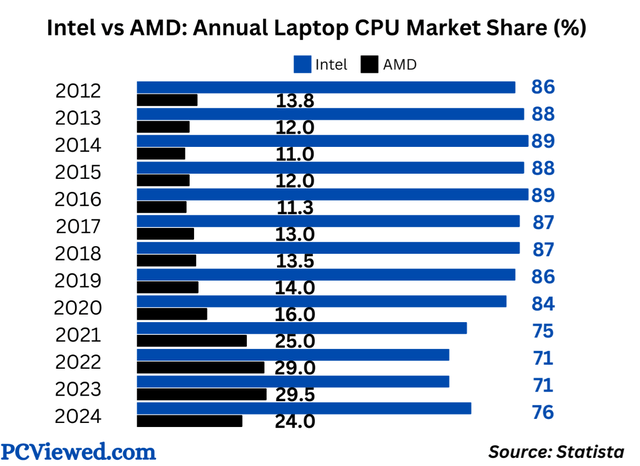

Just as AMD has continually taken market share from Intel in PCs, I believe they will also gain a significant share in AI PCs. As shown below, AMD’s PC market share has grown from 13.8% in 2012 to 24% in 2024.

AMD PC CPU Market Share (Statista)

The AI PC market will see significant growth in 2024 and 2025. Qualcomm (QCOM) initially took the lead with an exclusive deal with Microsoft in 2024, but in the future, all five companies will be competing for market share: Qualcomm, Apple (AAPL), AMD, Intel, and Nvidia.

AMD’s Ryzen AI300 is the company’s flagship product in this market. Boasting an estimated 50 TOPS of performance, it is the company’s third generation processor that has contracts with OEMs such as Acer, ASUS, Lenovo, and HP.

Although Arm Holdings (ARM) chips are energy (battery) efficient, the PC market is currently dominated by X86 processors with Intel and AMD holding over 80% market share. AMD is confident that X86 processing will hold its own, but has made the smart move to also manufacture ARM-based chips from 2025. It makes no sense to fall behind when users want longer battery life.

What’s more, advances in ARM’s AI and chip manufacturing techniques could make it even more powerful and energy efficient.

Apple was a pioneer, replacing Intel CPUs with ARM-based SOCs (System on Chip) over four years ago, and Qualcomm followed suit with its Snapdragon series, with the company’s CEO betting that 50% of PCs will run on the ARM architecture.

Weaknesses

AMD has struggled to generate strong margins, with GAAP operating margins stagnating in the high single digits and adjusted operating margins stagnating below 20%. AMD’s products lack pricing power, with even its new AI GPUs selling for 50% of the price of Nvidia’s Hopper series. Similarly, client and gaming operating margins are at 6% and 15%, respectively, and have been cleared of excess inventory. The client, gaming and embedded segments are cyclical, with little product differentiation, excess inventory and markdowns. These still account for 50% of AMD’s revenue, impeding growth and valuation.

Going forward, we expect these to recover and, overall, we expect adjusted margins to be around 22% to 24% in 2025 and 2026 as the gaming and embedded segments return to growth.

In server CPUs, AMD’s biggest competitor is struggling incumbent Intel, but in GPUs it competes with Nvidia for more than 90% market share.

There are three major competitors for PCs: Qualcomm, Apple, and Nvidia. There is optimism about AI PCs, but they may not come to fruition. There are limitations to what AI can do locally and it requires serious computing power from the cloud.

Investment projects and evaluation

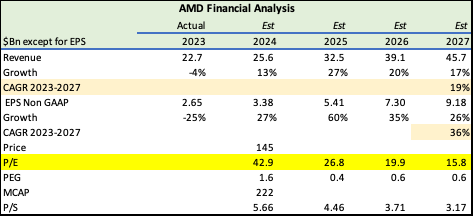

We’ve made a small adjustment to our previous model. We had expected a faster recovery in 2024, but were a bit more conservative until 2027. Instead, the analyst consensus forecast now calls for a significant improvement over the next three years. Overall, the differences are minor.

AMD Predictions (AMD, Seeking Alpha, Fountainhead)

AMD is cheap at 43x 2024 earnings, assuming 36% growth over the next four years. By 2027, the P/E falls to 16x and the PEG ratio to 0.6x. It’s also reasonable at a P/S valuation of 5.7x for a company growing 19% in the world’s fastest growing sector right now, where it’s supply constraints, not demand, that are driving down revenue.

It has firmly established itself in the number two position in terms of market share for AI data centers, a position that is enviable.

Valuation aside, AMD has proven to be an extremely tenacious competitor, taking 24% of the CPU server market from rival Intel, 12 times its size, in just seven years. Moreover, the company was dealing with cyclical changes in the PC and gaming market, and post-COVID inventory glut by 2024. The company’s share of the CPU server market will only grow. In GPU, its MI300x series is a strong competitor on memory strength. AMD will continue to slowly take share in this market, starting with less than 5% market share and only having to work its way up.

Nvidia can’t supply 100% of the market. AMD will address the part of the market that doesn’t require large compute workloads at about 50% of Nvidia’s price. The acquisition of Silo AI is a great move to strengthen our AI and software capabilities. Silo AI’s team has extensive expertise in developing AI solutions and large language models for major customers such as Allianz (OTCPK:ALIZF), Ericsson (ERIC), Finnair (OTCPK:FNNNF), Nokia (NOK), and Unilever (UL). This will enable AMD to compete with Nvidia’s CUDA and provide a seamless and comprehensive hardware and software package to hyperscalers and CSPs.

I own Nvidia and AMD and have bought and recommended Nvidia in July 2023 and March 2023 and strongly believe they will both perform very well.